For many SaaS founders, the seed stage is the most decisive — and the most often misunderstood — phase of their company's journey. What is seed-stage SaaS exactly, and how does it differ from pre-seed or Series A? Many founders reduce the seed phase to a fundraising question and miss that it's simultaneously about market validation, team-building and early product development. This article lays out the fundamentals, walks through the metrics that matter, compares funding instruments and gives practical guidance for planning your next growth steps.

Key Takeaways

| Point | Details |

|---|---|

| Define the seed stage clearly | Seed sits between pre-seed and Series A and focuses on MVP development plus first market validation. |

| Prepare KPIs for investors | MRR, churn and growth rate are the decisive numbers investors check in seed conversations. |

| Pick the instrument for your market | In DACH, the convertible loan (Wandeldarlehen) is the seed standard; SAFEs dominate the US. |

| Deploy capital with focus | Seed money belongs in product improvement, customer acquisition and building a scalable core team. |

| Plan Series A early | If you target Series A, you must build measurable progress and scalable processes already in the seed phase. |

What is seed-stage SaaS?

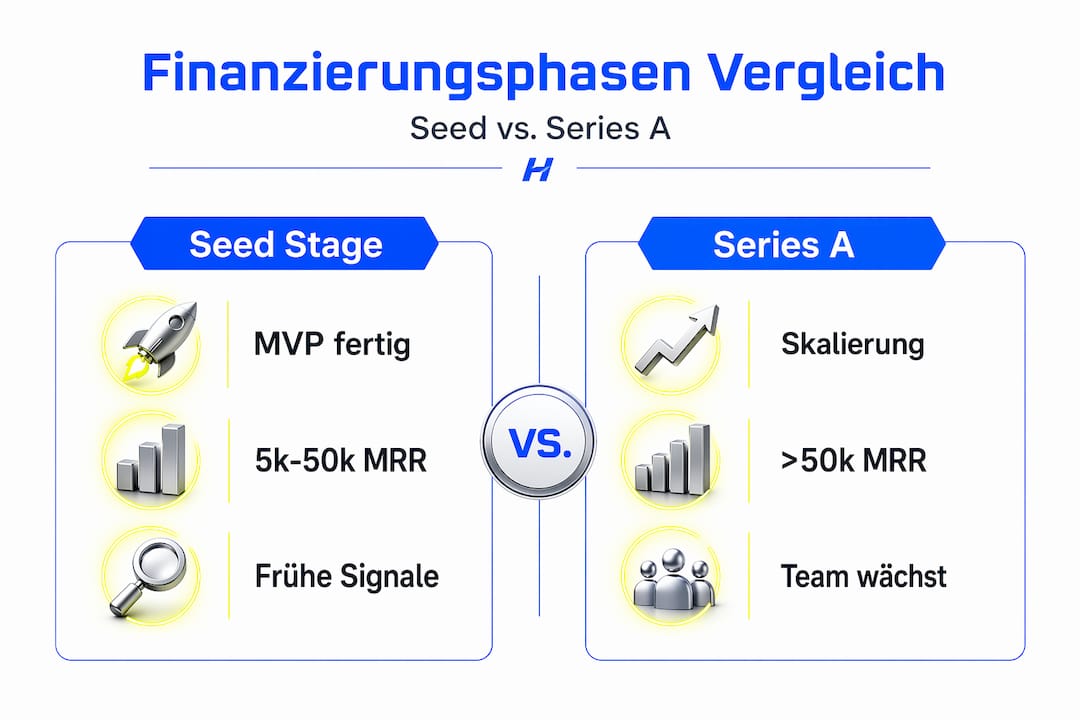

The seed stage is the first significant institutional funding round for a SaaS startup. Seed means MVP refinement, winning early customers and generating product-market-fit signals. In contrast to pre-seed — where the startup often consists only of an idea and an early prototype — seed is about proving market reality.

The term describes the phase well: a seed has been planted, but the fruit isn't visible yet. The startup has a product, early users and a team, but no fully established sales channel or proven business model.

Pre-seed vs. seed vs. Series A

The three phases differ fundamentally in maturity, funding size and expectations:

| Phase | Typical state | Funding range (typical) | Focus |

|---|---|---|---|

| Pre-seed | Idea, first prototype | €50k–500k | Team-building, first product work |

| Seed | MVP in place, first users | $500k–5M | Market validation, product maturity, growth |

| Series A | Proven business model | $5M–20M | Scaling, expansion |

Ranges are rough and vary widely by year, geography and sector — orientation, not hard rules.

Pre-seed focuses on very early development, while the seed phase is far more oriented towards reality-check and market validation. That's the crucial difference many founders only understand too late.

Typical traits of a seed-stage SaaS startup

SaaS startups in the seed phase share characteristic traits:

- A working MVP that solves real customer problems

- First paying customers, or at least active users with measurable usage

- A small core team of two to eight people

- First product-market-fit signals — even if PMF isn't fully proven yet

- Clear hypotheses about target market, pricing and customer acquisition

Seed investors evaluate mostly the team, market opportunity and early signals — not a fully established business model. That gives founders room to manoeuvre, but it also creates a clear expectation: you have to show you can learn fast.

KPIs and funding instruments in the seed phase

When you talk to investors, you have to speak the language of metrics. SaaS KPIs like MRR and ARR, plus customer retention, are decisive because the business model is built on recurring revenue. A one-off revenue spike doesn't impress anyone; consistent retention and growth do.

The KPIs that matter in investor conversations

Typical SaaS KPIs for investors in the seed phase sit in the following ranges:

| KPI | Rough seed-phase range | Why it matters |

|---|---|---|

| MRR (Monthly Recurring Revenue) | €5k–50k | Base for revenue planning and growth tracking |

| ARR (Annual Recurring Revenue) | €60k–600k | Yearly revenue derived from MRR |

| Monthly growth | ~15–30% (aspirational) | Evidence of market traction and demand |

| Churn rate | A low single-digit % monthly | Customer retention and product value |

| CAC (Customer Acquisition Cost) | Segment-dependent | Efficiency of the go-to-market motion |

These are illustrative ranges, not benchmarks to hit exactly — they vary widely. "Monthly growth of 15–30%" is an aspirational early-stage pace, and healthy B2B SaaS churn usually sits well below 5% monthly; for B2B, 1–2% monthly is a more meaningful target.

Despite the MRR/ARR focus, retention and churn are the metrics that often decide investments. A startup with 30 customers and 2% monthly churn is more attractive than one with 60 customers and 12% churn.

Pro tip: Before every investor conversation, prepare a simple KPI table showing the MRR trajectory over the past six months, churn rate and customer count. Investors always ask for these numbers — having them ready signals professionalism.

Funding instruments: SAFE, convertible note — and the DACH reality

US-centric advice tells you the SAFE (Simple Agreement for Future Equity) is the default: no interest, no repayment obligation, converts to equity at the next priced round — fast and founder-friendly. That's true in the US, where SAFEs dominate seed.

In Germany and DACH, the picture is different, and it matters:

- The convertible loan (Wandeldarlehen / CLA) is the de-facto standard for seed and bridge financing here — fast to sign, no company valuation required up front, and typically no notary until the eventual conversion (the capital increase, which German GmbH law does require to be notarised).

- A zero-interest instrument (the SAFE's signature feature) can actually create a German tax problem: tax authorities may treat an interest-free loan as a deemed taxable benefit, so DACH convertible loans usually carry a modest interest rate by design. The "no interest" advantage that makes SAFEs attractive in the US is, in Germany, a reason to be careful.

- SAFEs exist in the German market but are far less established than CLAs, and German-law adaptations are still maturing.

So the practical takeaway isn't "SAFE good, convertible note bad" — it's: in the US, default to a (post- or pre-money) SAFE; in DACH, expect a convertible loan with a cap/discount and modest interest, and get it reviewed by a startup lawyer. Whichever you use, the instrument shapes not just the cap table but the pressure: a loan with a hard maturity date forces the next round by a deadline, ready or not.

This is fundraising context, not legal or tax advice — have funding-instrument and tax specifics reviewed by a qualified advisor.

Strategy and economics in the seed phase

Once the capital lands in your account, the actual work begins. Seed money is for improving the product, building the core team and gathering the data needed to prepare for Series A. That sounds simple, but in practice it's a constant prioritisation exercise.

Deploy capital with focus

The most common misconception in the seed phase is that more capital equals more room. In reality, lots of capital often just creates more distraction. Typical seed-phase spend categories:

- Product development: bug fixes, feature work driven by customer feedback, technical scalability

- Customer acquisition: first paid channels, content build-up, first sales processes

- Team-building: key hires like first sales rep, designer or backend engineer

- Infrastructure: privacy-aware data handling, CI/CD pipelines, monitoring

Building a production-ready SaaS in the seed phase doesn't mean shipping every feature — it means shipping the right features cleanly. Tech debt accumulated in seed becomes a brake on Series A.

Structuring go-to-market and hiring

A scalable go-to-market motion doesn't start with a big budget — it starts with clear hypotheses. Which customer segments react strongest? Which channel produces the lowest acquisition cost? You have to answer these questions in seed, not in Series A.

Pro tip: Define a measurable milestone for each spend category before you spend the money. For example: "We invest €20k into performance marketing to test whether CAC stays below €300." Without that frame, you burn capital without learning anything.

Planning the next round

Seed-stage SaaS startups plan their funding so that they can show measurable progress and scalable processes by the time of Series A. Concretely, that means: you need not just revenue numbers, but processes, documentation and a team that functions without you, the founder.

A scalable SaaS architecture isn't a nice-to-have, it's a prerequisite. Series A investors run technical due diligence. If they then find spaghetti codebases without tests and without monitoring, trust evaporates fast.

Common traps to avoid

The most frequent seed-phase mistakes are predictable and avoidable:

- Building too many features before validating the core value

- Growing the team too aggressively and pushing up burn rate

- Not measuring KPIs regularly — no data basis for decisions

- Starting investor conversations without a clear narrative or current numbers

Investor types and funding sizes

Not every seed round is the same. Seed rounds usually span $500k to $5M as the first significant institutional capital round, with size depending heavily on market, investor type and geography.

Seed-phase investor types

| Investor type | Typical ticket | Focus | Value for startups |

|---|---|---|---|

| Angel investor | €25k–200k | Individuals with industry knowledge | Network, mentoring, speed |

| Micro VC | €200k–1M | Specialised fund for early phases | Structured process, follow-on investments |

| Seed fund | $500k–5M | Institutional seed-stage fund | Larger network, Series A contacts |

The choice of investor has strategic consequences. An angel with industry knowledge in your B2B SaaS segment can open doors that a generalist fund can't. At the same time, micro VCs often bring more structured processes, which is valuable for inexperienced founders.

Regional differences: US vs. DACH

In the US market, seed rounds are larger on average and valuation expectations are higher. In Germany and DACH, seed rounds are typically structured more conservatively, with greater focus on profitability and less appetite for years of loss-financing.

For SaaS founders in Germany that means: you have to show earlier that your business model is built towards profitability. The classic Silicon Valley "growth at any cost" strategy is harder to fund here. DACH investors also pay close attention to GDPR compliance, which puts technical requirements on the product.

A few characteristics that set the DACH seed market apart:

- Lower average valuations at comparable traction

- Higher expectations around legal and data-protection-compliant product structure

- Stronger preference for B2B over consumer SaaS

- More weight on demonstrated revenue rather than pure user growth

If you want to start with privacy-aware foundations, it's worth building these requirements in already in the seed phase — not when the first enterprise customer asks for them.

My take on the seed stage

I've worked with many founders during the seed phase, and the most common observation is this: most underestimate how much clarity investors expect, and how little capital is actually needed to produce that clarity.

What I've learned in practice: seed is not about shipping as much as possible as fast as possible. It's about answering three questions. Who buys the product? Why do they stay? How do you get more of them? If you can answer those three questions with data, you've understood the seed phase.

Another pattern I keep seeing: technical debt is chronically underestimated in seed. Founders build fast because speed is treated as a virtue. But a bad database schema in seed costs three engineer-months to fix in Series A. That's lost capital and lost time.

My advice to every SaaS founder in seed: invest early in architecture and test coverage, even when it feels like overhead. And pick investors not by ticket size but by strategic fit. An angel with ten customer contacts in your target segment is often more valuable than €500k without a network.

— Anna

How H-Studio supports founders in the seed phase

For SaaS founders in the seed phase, the technical foundation isn't a downstream task. It determines how fast you can scale, how your product holds up in Series A due diligence and whether your architecture can answer privacy and security questions. H-Studio Berlin builds that foundation with you, not after you.

As an engineering partner for founders H-Studio Berlin takes on the full technical execution — from architecture through backend and frontend to deployment and monitoring. Typical projects are SaaS MVPs, customer portals and scalable platforms that build instant trust with investors and enterprise customers.

If you want to know which architecture is right for your product, Modern Web Stack is the natural entry point — or directly an Architecture Sprint as the first paid step before the MVP build.

FAQ

What does seed stage mean for a SaaS startup?

The seed stage is the first significant institutional funding round, in which a SaaS startup refines its MVP, wins its first paying customers and produces product-market-fit signals. It sits between pre-seed and Series A.

How much capital is raised in a seed round?

Seed rounds are typically $500k to $5M, with size depending on market, geography and investor type. In DACH the amounts are usually slightly smaller than in the US.

Which KPIs are decisive for SaaS investors in seed?

Investors look at MRR between €5k and €50k, monthly growth of 15–30 percent, churn below 5 percent and customer acquisition cost. These numbers act as sanity checks in investor conversations.

What's better for seed funding: SAFE or convertible note?

It depends on your jurisdiction. In the US, SAFEs are the fast, no-interest default. In DACH, the convertible loan (Wandeldarlehen) is the standard — and a zero-interest structure can create German tax issues, so CLAs usually carry modest interest. Get either reviewed by a startup lawyer.

How do angel investors differ from seed funds?

Angel investors typically invest €25k–200k and bring personal networks and industry knowledge. Seed funds invest $500k–5M, offer more structured processes and often access to Series A investors.

Recommended reading

- Scalable, GDPR-safe SaaS launch: tips for founders — privacy-aware foundations for go-to-market

- Scalable systems: why B2B SaaS plans early — the architecture Series A due diligence checks

- Scalable software architecture: benefits for founders & CTOs

- Architecture Sprint — structured architecture review with a fixed scope, before the MVP build

Edited and fact-checked by Anna Hartung.